The New Iran War and the Day the Extractives Order Changed

Image: RTK Grafika

What The February 28 US-Israeli Strikes Mean for African Resource Economies

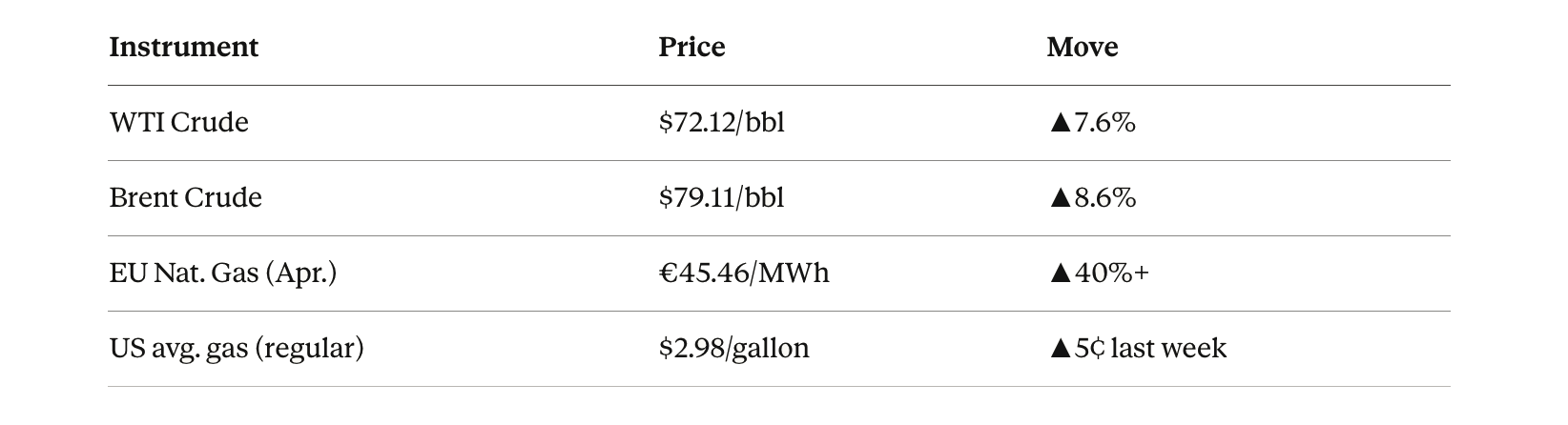

UPDATE — 2 March 2026: Energy markets opened the week with sharp confirming moves. U.S. WTI crude surged 7.6% to $72.12/barrel; Brent climbed 8.6% to $79.11. European natural gas futures spiked over 40% after QatarEnergy halted LNG production. Tanker traffic through the Strait of Hormuz dropped sharply following satellite navigation disruptions and confirmed vessel attacks. Saudi Arabia's Ras Tanura oil refinery was shut down after intercepting Iranian drone strikes.

⟁ OPINION | Tina Abelshauser, Arno Saffran, Sat 28 Feb, 2026At dawn on Saturday, 28 February 2026, the United States and Israel launched coordinated strikes across Tehran, Qom, Isfahan, Kermanshah, and Karaj — the largest American military operation in the Middle East since the 2003 invasion of Iraq. Within hours, Iran's Revolutionary Guards retaliated simultaneously against four U.S. military installations spanning four Gulf Arab states. For the first time in history, Iranian ballistic missiles struck the capitals that host the world's most critical military and energy infrastructure at the same moment.

This is not a conventional oil shock. It is a systemic rupture — one that tests every assumption on which global energy security, critical mineral supply chains, development finance, and long-term extractive investment in Africa has been built.

Three Strikes, Three Precedents: Venezuela, Iran I, and Iran II

Venezuela: The Rehearsal

In January 2026, U.S. forces participated in the incursion that led to the capture of former Venezuelan President Nicolás Maduro. Market reactions were subdued — Venezuela's heavily sanctioned, heavily degraded production base meant the immediate supply shock was manageable. But the precedent was seismic: for the first time in the modern era, Washington deployed kinetic force against a sovereign OPEC petroleum producer in the Western Hemisphere. Maduro art the time of writing (02.28.2026) is seeking a dismissal of charges, with his claim the US blocked legal defence funds.

For African resource economies, this carried an immediate message: the protection of sovereign resource rights can no longer be taken for granted. A state's hydrocarbon or mineral wealth is now, explicitly, a strategic variable in U.S. foreign policy calculus — and compliance or non-compliance with Washington's strategic interests may invite consequences beyond the economic.

Iran I (June 2025): The Warning Shot

The June 2025 U.S. strikes on Iranian nuclear facilities were surgical and contained. Iran struck Al Udeid Air Base in Qatar in retaliation — with advance warning. Markets absorbed the shock. But the structural damage was deeper than the flat price movement suggested. War-risk insurance premiums for Gulf-transiting vessels doubled, from 0.2–0.3% of hull value to 0.5% — with panic-peak quotes touching 1.0% — translating to $0.10–0.15 per million BTU in structural cost for Q-Flex LNG carriers. The Strait of Hormuz had not been physically blocked, but it had been re-priced.

Iran II (February 2026): Breakdown

February 28th air strikes are categorically different on every dimension that matters to our clients and their investment decisions.

Scale: June targeted nuclear facilities across one thematic category. February struck leadership compounds, intelligence headquarters, and military-industrial infrastructure simultaneously across six cities. The U.S. military is publicly planning for 'several days of attacks.' This is the largest American military mobilization in the region since 2003.

Intent: June sought degradation. February explicitly seeks transformation — regime change. President Trump's call for Iranians to 'take over your government' and Israel's characterization of the operation as targeting the 'existential threat' are not diplomatic formulations. Markets must now price the probability of Iranian state collapse alongside the probability of Iranian military escalation.

Retaliation scope: In June, Iran struck one base with advance warning. In February, the IRGC declared all American and Israeli assets across the entire Middle East legitimate targets — and struck simultaneously in Qatar, the UAE, Bahrain, Kuwait, and Jordan. One person was killed by debris in Abu Dhabi after UAE intercepted incoming ballistic missiles. A senior Iranian official told Al Jazeera: 'there are no red lines after this aggression.'

The difference between June and February is the difference between a thunderstorm and a climate event. One passes. The other reshapes the terrain permanently.

The Hormuz Equation

Beyond oil price headlines, every market commentary this weekend will focus on Brent crude — which closed Friday at $72.48, already carrying a geopolitical premium from weeks of military buildup. Analysts expect a significant war premium when Asian markets open Sunday evening, with estimates ranging from a 5–10% price increase under a contained scenario to above $100 per barrel if the Strait of Hormuz faces partial disruption.

Tanker traffic has dropped sharply as of Monday. Satellite navigation systems in the strait have been disrupted (confirmed by Kpler data). The U.K. Maritime Trade Operations Centre reported attacks on multiple vessels and issued warnings of elevated electronic interference. A bomb-carrying drone struck a Marshall Islands-flagged tanker in the Gulf of Oman, killing one mariner.

But the flat crude price is the least instructive number. The more consequential analysis runs through the structural layers beneath it.

The Chokepoint in Numbers

Monday's (March 2nd, 2026) surge is within the $5–$10/barrel fear-premium analysts had projected. The more consequential data point is European gas — ICE April delivery futures surged after QatarEnergy confirmed it was halting LNG production, citing the conflict. Qatar is Europe's critical replacement for Russian pipeline gas. That supply line is now in question.

Pass-through to consumers: A $10/barrel crude increase typically adds ~$0.25/gallon at U.S. pumps within 20 days. For Europe, a sustained $15/barrel rise could add 0.5 percentage points to consumer prices.

One moderating factor: Political pressure from the Trump administration ahead of November's midterm Congressional elections is expected to constrain maximum escalation, with some analysts forecasting a return to $65–$70/barrel after the near-term spike — contingent on de-escalation.

This is not simply an oil story. The ammonia and urea that flow through Gulf ports — derived from Qatari and Saudi natural gas — feed fertiliser supply chains that reach every agricultural economy in sub-Saharan Africa. Morocco's phosphate export routes are sensitive to broader Red Sea and Arabian Sea freight risk. A sustained disruption to Hormuz transit would transmit inflationary pressure directly into food security across the continent within a single growing season.

Iran's parliament approved a motion to close the Strait following June's strikes — a motion the Supreme National Security Council did not activate. Tehran conducted live-fire naval exercises in the Strait as recently as February 17, 2026, temporarily closing sections of the channel. The IRGC maintains fast-attack boats, anti-ship missiles, naval mines, and semisubmersible craft specifically designed for asymmetric warfare in these waters. Even a 20–30% flow reduction through mining or harassment — Scenario B in our analysis below — would send Brent above $100. Full closure, however brief, enters territory no economic model has tested.

Why Critical Minerals are Africa's Hidden Exposure — and Hidden Opportunity

Africa holds a disproportionate share of the world's most strategically important mineral reserves. The Democratic Republic of Congo accounts for approximately 70% of global cobalt production and holds 71% of proven reserves. The continent produced 4.2 million tonnes of copper in 2025, driven by the DRC and Zambia. Zimbabwe, Namibia, and Mozambique have tripled lithium output between 2021 and 2025. South Africa dominates platinum group metals. Morocco holds the world's largest phosphate reserves. The continent's aggregate mining output value grew from $480 billion in 2021 to over $620 billion in 2025 — a compound annual growth rate of 6.5%, outpacing global averages.

Global demand trajectories amplify this position further. The International Energy Agency projects copper demand rising 50% by 2040, nickel and cobalt demand doubling, and lithium demand growing eightfold. Demand for critical minerals overall is forecast to increase five-fold by 2035 compared to 2023 levels. Africa sits at the structural centre of this transition — and the Iran crisis intensifies the urgency with which every major industrial power is seeking to secure long-term supply.

Geopolitical Re-pricing of the Supply Chain

The great-power scramble for African minerals has been building for years. China's foreign direct investment in Africa surged 118.8% year-on-year to $3.96 billion in 2023, with mining accounting for 22% of total Chinese investment. Chinese policy banks issued $24.9 billion in Belt and Road-linked mining loans in the first half of 2025 alone — a record pace. China controls 68% of the DRC's Sicomines joint venture, dominates cobalt refining globally, and produces 60% of renewable energy equipment.

The United States has responded with accelerating urgency. At the U.S.-hosted Critical Minerals Ministerial on 4 February 2026 — just 24 days before the Iran strikes — more than fifty countries gathered at the State Department to announce a preferential trading bloc with coordinated price floors. The U.S.-backed Orion Critical Mineral Consortium signed a memorandum of understanding with Glencore to acquire a 40% stake in Mutanda Mining and Kamoto Copper Company in the DRC, in a $9 billion transaction. The U.S. Development Finance Corporation is managing a continental portfolio exceeding $13 billion in mining, processing, and transport infrastructure. The $553 million Lobito Corridor rail investment — connecting Zambia and Angola — is explicitly designed to create a transcontinental mineral export route that bypasses chokepoints.

“At least 13 African countries have enacted export restrictions since 2023 — cobalt quotas in the DRC, lithium bans in Zimbabwe and Namibia, raw mineral bans in Malawi. Africa is beginning to exercise mineral sovereignty. The Iran crisis sharpens this leverage.”

The Iran crisis does not slow this scramble. It accelerates it. Military conflict in the Middle East reminds Washington, Brussels, Tokyo, and Seoul that diversifying away from geopolitically volatile supply chains is not optional. Africa is the alternative. The question is on whose terms African producers engage.

The Iran Risk Transmission to African Mineral Economies

First, shipping and freight costs: sustained conflict raises insurance premiums and freight rates across all major shipping routes, including those serving African mineral export corridors. This compounds already elevated war-risk premiums — from 0.2–0.3% pre-June 2025 to potentially unquotable levels in the current escalation — directly into the economics of every junior mining company shipping concentrate out of a sub-Saharan port.

Second, development finance: as global risk appetite contracts, Development Finance Institutions adjust their risk ratings for extractive projects in conflict-adjacent and geopolitically uncertain regions. Projects in pipeline may face renegotiation, delay, or withdrawal of concessional facilities.

Third, offtake pressure: a crisis of this magnitude creates intense demand from industrial buyers to lock in long-term offtake agreements for critical minerals at terms that, under normal conditions, African producers would resist. The urgency of Western industrial buyers — seeking to reduce Hormuz and China dependency simultaneously — creates opportunities, but also risks of underselling. This is precisely where Unamine's commercial intelligence and diplomatic positioning adds direct value.

Fourth, sovereign revenue pressure: governments managing fuel subsidy budgets will face acute pressure as import costs rise. Those without robust extractive governance frameworks — transparent contracts, revenue stabilisation mechanisms, independent oversight — will be disproportionately exposed. Those with such frameworks will be better positioned to attract emergency liquidity and renegotiate from strength.

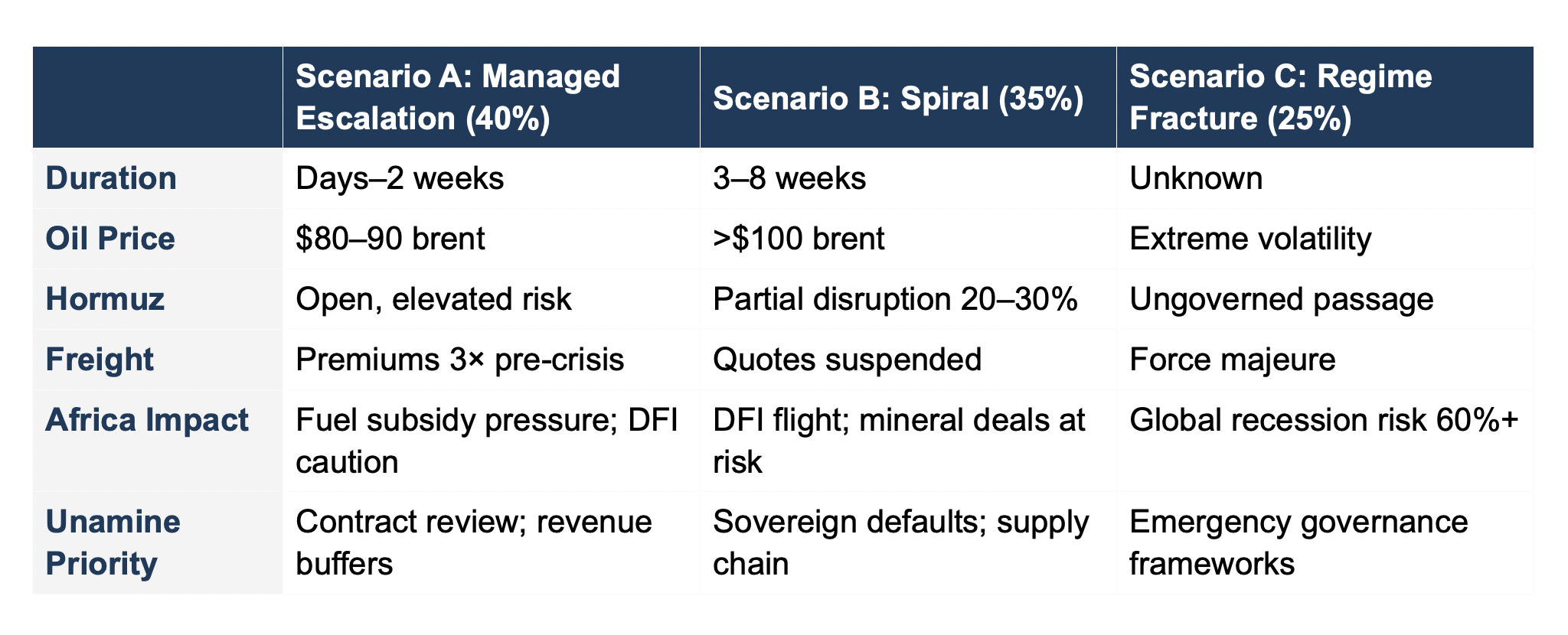

Scenario Analysis: The Next 90 Days

Scenario probabilities reflect Unamine's internal assessment as of 28 February 2026. Subject to revision as military operations develop.

Scenario A: Sustained Strikes, Managed Escalation (40% probability)

The U.S. and Israel conduct several days of operations, degrade Iranian military and nuclear infrastructure significantly, and a ceasefire is brokered through Omani or Qatari backchannel mediation. Hormuz remains open but under substantially elevated threat.

Confirmed near-term movement toward $79–$80 already underway; upper bound of $90 if infrastructure attacks continue. Add note: some forecasters project return to $65–70 after near-term spike under de-escalation.

For African mineral economies: DFI caution increases but does not freeze. Offtake renegotiations accelerate. Fuel subsidy pressure is real but manageable with fiscal headroom. Unamine's Phase One positioning — commercial diplomats embedded with OEMs and EPCs — becomes immediately valuable as industrial buyers seek alternative, stable supply relationships.

Scenario B: Escalation Spiral (35% probability)

Iranian retaliation produces meaningful U.S. casualties. Proxy networks — Hezbollah, Kata'ib Hezbollah, the Houthis — activate simultaneously across Lebanon, Iraq, and Yemen. Hormuz faces partial disruption through mining or harassment, removing 20–30% of flow. Brent spikes above $100. War-risk underwriters stop quoting. Gulf airspaces remain intermittently closed, stranding aircraft and supply chains. Expatriate outflows from the Gulf exceed 5%, crippling refinery and port operations. Global recession risk rises sharply.

For African mineral economies: DFI investment flight accelerates. Existing mineral deals — including U.S.-DRC arrangements — face operational disruption from logistics breakdown. Copper concentrate stuck in congested or uninsurable ports drives spot price volatility. This is the scenario in which Unamine's governance and commercial intelligence mandate is most acutely tested — and most acutely valuable.

Scenario C: Regime Fracture (25% probability)

The protest movements that erupted across Iran in January 2026 — the largest since 1979, met with massacres estimated to have killed between 3,000 and 36,500 people — reignite under the cover of external strikes. Elements of the Iranian military refuse to fight on two fronts. The regime fragments rather than falls cleanly. Hormuz becomes ungoverned rather than strategically controlled — contested by IRGC remnants, Iranian naval factions, and U.S. warships simultaneously. No state is issuing mining authorisations or offtake guarantees in that environment.

Oil volatility in this scenario exceeds anything since the 1979 revolution. The Columbia University Center on Global Energy Policy warned earlier this month that even a short-term price spike would 'jeopardize the foundations of non-oil growth and diversification' across the GCC — growth the IMF estimates at 3.7–3.8% and that Citi projected would accelerate to 4.5% in 2026. That diversification progress is now directly threatened.

The Energy Transition and Frontier Mining

The world is in the midst of an energy transition driven partly by the desire to reduce dependence on geopolitically volatile fossil fuels. Yet the military conflict over Iran — itself a fossil fuel power story — is simultaneously driving up near-term price signals that incentivise more fossil fuel production, while generating the geopolitical instability that makes long-term transition investment harder to plan, finance, and de-risk.

For junior frontier mining companies — the clients Unamine's Phase Two model is explicitly designed to serve — this double bind is acutely relevant. Demand for the minerals they are developing is structurally growing. The IEA's Global Critical Minerals Outlook 2025 projects that by 2040, 4.5 times as much lithium and 2.3 times as much graphite will be needed globally. Copper demand will be 50% higher. Yet the capital environment, shipping logistics, insurance availability, and DFI risk appetite that make it possible to get a junior project from exploration to production in a frontier jurisdiction are all under acute pressure today.

The companies that will emerge from this crisis in strong positions are those that entered it with three things: transparent, internationally recognised contracts; relationships with OEMs and EPCs that can move offtake agreements and EPC procurement packages quickly when windows open; and governance structures that allow them to demonstrate responsible stewardship of mineral assets to DFI partners who need political cover for continued engagement.

What Extractives Operators Should Do in the Next 30 Days

Operators should conduct an immediate audit of Gulf-transiting supply chain exposure — particularly for components, materials, or services where single-source dependency on Gulf-region suppliers exists. Engineering procurement schedules for projects with Gulf-origin inputs should be stress-tested against 30-, 90-, and 180-day disruption scenarios. Identifying African-origin alternative supply lines with sufficient development maturity to be credible substitutes in accelerated procurement discussions.

For Junior Frontier Mining Companies (Phase Two Pipeline)

This is not a moment to pause. It is a moment to get governance right, get relationships right, and get documentation right. Companies with transparent, internationally arbitrable contracts and clear beneficial ownership structures will be dramatically better positioned to access emergency DFI liquidity, attract offtake buyers operating under industrial urgency, and withstand the scrutiny that comes when Western governments are actively looking for responsible supply chain partners to champion politically. Companies without these things should treat this month as a governance sprint, not a wait-and-see period.

For Host Governments in Mineral-Producing Countries

Governments should monitor three specific pressure points. First, fuel subsidy exposure: as import costs rise, the fiscal headroom required to maintain energy subsidies will tighten rapidly. Governments with diversified revenue bases from well-governed mineral royalties are better positioned. Second, offtake pressure: Western industrial buyers will move quickly to lock in long-term mineral supply agreements on terms that reflect their urgency rather than the producer's leverage. Governments and national mining companies should not sign in the next 30 days without independent commercial intelligence on whether current market conditions represent a floor or a ceiling. Third, DFI relationships: the institutions funding African infrastructure are themselves under pressure from their own boards to demonstrate responsible deployment. Governments that can demonstrate governance credibility will access capital that others will not.

The Climate Metaphor Has Run Out of Time

For the past eight months, the most sophisticated analysis of Gulf energy risk has employed the metaphor of climate change: gradual accumulation of structural risk, the need for adaptation over time, the asymmetric consequences of delayed action. That metaphor assumed that diversification, governance improvement, and supply chain rebalancing could proceed at the pace of normal business cycles.

February 28, 2026 has ended that assumption. Missiles struck the capitals hosting the world's most important military and energy infrastructure simultaneously. Iran declared no red lines. The United States declared regime change as its objective. The Strait of Hormuz — through which 20% of the world's oil and gas, all of Qatar's LNG, and the ammonia and urea that feed African agriculture flow — is under active threat for the first time since the Iran-Iraq tanker wars of the 1980s.

For the extractives sector, and for every economy whose development depends on it, the question is no longer whether to adapt. It is whether you have already adapted — and if not, whether you can move fast enough. Unamine was built for exactly this environment: to provide the commercial intelligence, diplomatic positioning, and governance infrastructure that turns resource endowment into development impact, regardless of what is happening in Tehran, Abu Dhabi, or Washington.

The world needs the minerals Africa holds. The crisis makes that need more urgent, not less. The opportunity is real. Capturing it requires the capacity to act with speed, credibility, and sovereign confidence — the three things Unamine is in the business of building.

References:

Forbes Intelligence (28 Feb 2026)

POLITICO (28 Feb 2026)

Oman Says Oil Tanker Targeted Off Its North Coast." Bloomberg, 1 March 2026.

Mealha, Q. "First oil tanker attacked in the Strait of Hormuz according to Oman." Euronews, 1 March 2026.

Kpler, Tanker Traffic Data (02 March 2026) https://x.com/Kpler

NB. All sources accessed March 02, 2026. URLs verified at time of publication. Unamine makes no representation as to the continued availability of external links.

How relevant and useful is this article for you?

★ 81

UNAMINE works across the mining & metals value chain, positioning people who form the critical bridge to early-stage relationships in complex regions.